Ref: TIL-CP-2026 · Validity: 30 Calendar Days

Authorized Channel Partner Proposal

Prepared by: TaxInLaw Technology Limited

Contact: taxinlaw@proton.me

Annual License Fee

₦120,000

per entity · per year · earn up to 30%

TAXINLAW TECHNOLOGY LIMITED

Authorized Channel Partner Proposal

Prepared by: TaxInLaw Technology Limited ("TaxInLaw" or "the Company")

Contact: taxinlaw@proton.me

Proposal Date:

Reference No.: TIL-CP-[YEAR]-[---] For: [Partner Firm Name] ("Prospective Partner")

Validity: Thirty (30) calendar days from date of issuance.

A NOTE BEFORE WE BEGIN

We believe the strongest business relationships are built on three things: clarity, transparency, and mutual accountability. This Proposal is our sincere and good-faith effort to lay out, in full, what a partnership with TaxInLaw looks like — what we bring to the table, what we're asking of you, how we'll compensate you fairly for your work, and how we'll both be protected when things don't go according to plan (because sometimes, they won't).

This is not a contract. It is an invitation — a structured, detailed invitation — to a commercial relationship that we believe can be genuinely valuable for both sides. The formal Channel Partner Agreement will follow upon your acceptance. But we want you to understand exactly what you're stepping into before you sign anything.

Read this carefully. Share it with your legal counsel if you wish. Ask us questions. We're building something together, and we'd rather you go in fully informed than be surprised later.

— TaxInLaw Technology Limited

SECTION I — WHO WE ARE AND WHAT WE'VE BUILT

1.1 Company Overview

TaxInLaw Technology Limited is a Nigerian-founded, cloud-native technology company whose singular focus is solving one of the most universally frustrating problems in Nigerian business life: tax compliance. We've built a proprietary SaaS (Software-as-a-Service) platform that consolidates what used to require multiple consultants, multiple spreadsheets, multiple software tools, and multiple sleepless nights before every FIRS deadline — into a single, secure, intelligently designed dashboard.

We are not a consulting firm that also has software. We are a technology company that has encoded expert Nigerian tax knowledge directly into software — so that the intelligence travels with your clients wherever they are, twenty-four hours a day, seven days a week, without a retainer invoice.

1.2 The Platform: What TaxInLaw Business Does

The TaxInLaw Business platform provides Nigerian companies — from nimble SMEs to large corporates and multinational group entities — with a unified workspace covering every major area of financial and tax compliance:

Tax Compliance & Advisory

- ›• Corporate Income Tax (CIT) computation, planning, and filing preparation under the Companies Income Tax Act (CITA) and the Finance Act (as amended)

- ›• Withholding Tax (WHT) tracking, rate management (5% / 10%), and remittance status monitoring

- ›• Value Added Tax (VAT) management at the statutory 7.5% rate with automatic taxable/non-taxable line-item distinction

- ›• Capital Gains Tax (CGT) recording on asset disposals — proceeds, cost base, and computed tax liability

- ›• Customs and Excise duty declaration tracking for import-dependent businesses

- ›• More Taxes module for jurisdiction-specific and industry-specific levies

Finance & Bookkeeping

- ›• Full income and expense transaction management with VAT and WHT fields natively embedded in every record

- ›• Payment method tracking (Cash, Bank Transfer, Cheque, POS/Card), approval trails, memo and voucher numbering

- ›• Real-time outstanding balance computation

- ›• Multi-currency support (NGN and USD)

Invoicing System

- ›• Professional invoice generation with full lifecycle management: Draft → Sent → Partially Paid → Paid → Void / Overdue

- ›• Automatic VAT computation on taxable line items (rate snapshotted at invoice creation for audit integrity)

- ›• Partial payment tracking with running balance-due calculations

- ›• Client detail snapshots and bank detail snapshots to ensure historical invoices remain permanently accurate

- ›• PDF generation and storage

HR & Payroll

- ›• Employee records with PAYE, pension (8%+), NHF, and other deduction configurations stored per employee via a flexible JSON configuration engine

- ›• Payroll run processing with gross pay, net pay, and deduction computation

- ›• Immutable payroll history snapshots for audit and dispute resolution

Insurance Ledger

- ›• Corporate insurance policy management across all major types: Group Life, Health, Motor, Marine, Fire, Professional Indemnity, NSITF, and more

- ›• Date-based policy status computation (Active / Pending / Expired)

- ›• Premium payment tracking by coverage period — with statutory deductibility and NSITF flags

Loans & Credit Facility Management

- ›• Full loan register across account types: Term Loans, Overdrafts, Credit Cards, Lines of Credit, Mortgages

- ›• Transaction ledger for every movement: Repayments, Interest Charges, Penalties, and Disbursements — each with a running balance snapshot

- ›• Auto-Pilot Interest Accrual: For loans configured with auto_accrue_interest = True, the platform can automatically post periodic interest charges, eliminating the risk of missed accruals in your financial statements

- ›• Connected-party loan flagging for transfer pricing and thin-capitalisation analysis

Fixed Asset Management

- ›• Complete fixed asset register across categories: IT, Furniture, Vehicles, Machinery, Electronics, Buildings, Land

- ›• Asset lifecycle tracking from Acquisition through Active use, Maintenance events, and eventual Disposal, Theft, or Loss

- ›• Maintenance log management with cost, provider, and status per maintenance event

- ›• Asset assignment and custody history tracking — who had what, and when

Investments Monitoring

- ›• Investment portfolio tracking covering Stocks, Bonds, and other instruments

- ›• Principal vs. current value visibility for gain/loss monitoring

Analytics & Reporting

- ›• Real-time financial statistics and KPI dashboard aggregated from Finance, HR, Invoices, and other modules

- ›• Data-driven insights without requiring a separate BI tool

News & Tutorials

- ›• Integrated regulatory news feed and curated tutorial content to keep Clients informed about FIRS updates, Finance Act amendments, and compliance deadlines

Notifications Engine

- ›• Event-driven in-platform notification system that alerts Clients to invoice status changes, subscription renewals, and critical compliance milestones

1.3 The Flagship Feature: The AI-Powered Tax Advisory Engine

We deliberately saved this for last in our platform overview because we want it to land with the weight it deserves.

The TaxInLaw Advisory Engine is the most sophisticated feature on the platform, and one of the most uncommon in the Nigerian market.

Here is what it does: A Client inputs their financial data — income, expenses, deductions, industry sector, residency status, turnover — and the Advisory Engine processes that information through a structured, rules-based artificial intelligence framework encoded directly from the Nigerian Companies Income Tax Act and the Finance Act (2023 edition). The engine then generates tailored, actionable tax advice — not generic disclaimers, but actual recommendations on Corporate Income Tax filing strategy.

The Client can select their advisory perspective:

- ›• CPA Strategy — computationally focused, optimized for accuracy and defensible deduction claims

- ›• Lawyer Strategy — structurally focused, emphasizing statutory interpretation and risk-managed filing positions

The engine does not replace a tax professional. What it does is give your Clients — the CFO of a mid-sized trading company in Lagos, the director of a petroleum services firm in Port Harcourt, the accountant of a growing manufacturing business in Kano — the kind of structured, law-based preliminary analysis that previously required booking an expensive appointment with a Big Four firm, all within their subscription, at any hour of any day.

This is the feature that answers the question every prospect will eventually ask: "But why TaxInLaw instead of just using a consultant?"

Because consultants go home. The TaxInLaw Advisory Engine does not.

SECTION II — THE CHANNEL PARTNER PROGRAM

2.1 Program Philosophy

TaxInLaw has chosen not to pursue a traditional, aggressive direct-sales model for its initial market expansion. Instead, we're building something more durable: a curated network of trusted, knowledgeable commercial partners — accounting firms, management consultants, marketing agencies, and aligned professional services organizations — who already have established relationships with the very businesses TaxInLaw is designed to serve.

This is not a referral link scheme. This is not an affiliate click-tracking program. This is a structured commercial partnership in which you, the Authorized Partner, are a recognized representative of TaxInLaw's product within your professional ecosystem — bringing credibility, local knowledge, and existing trust to the sales process in ways that no digital ad campaign can replicate.

We call this program internally the TaxInLaw Track Program — named after our commitment to giving every Partner a clear, transparent, real-time track record of every sale, every client, every commission, and every renewal, visible through the TaxInLaw Partner Dashboard.

2.2 Who We're Looking For

We welcome applications for Partner status from:

- ›• Accounting and Audit Firms — who serve clients that are precisely the businesses TaxInLaw serves. The conversation is already happening; TaxInLaw simply becomes a tool recommendation embedded in your advisory relationship.

- ›• Management and Business Consulting Agencies — who engage with business owners, CFOs, and corporate executives on operational and strategic matters where tax compliance is always on the agenda.

- ›• Marketing and Business Development Agencies — with established B2B networks, corporate client bases, or digital reach within the Nigerian business community.

- ›• Legal Practices (Corporate and Commercial) — whose clients regularly encounter tax-related matters in the course of corporate transactions, contract reviews, and business structuring.

- ›• Other Professional Services Organizations — that interface with Nigerian businesses in a trusted advisory capacity.

2.3 Eligibility Requirements

To be considered for the Program, a Prospective Partner must:

- ›Be a duly registered entity under Nigerian law, with a valid CAC registration number;

- ›Designate a named, identifiable primary point of contact accountable for all Program communications;

- ›Consent to TaxInLaw's standard onboarding verification process;

- ›Have no known history of commercial fraud, financial misconduct, or regulatory sanction in any jurisdiction;

- ›Agree, in principle, to the terms set out in this Proposal pending formal Agreement execution.

TaxInLaw reserves the unconditional right to decline any applicant at its sole discretion, without obligation to provide reasons.

SECTION III — COMMISSION STRUCTURE & PARTNER TIERS

3.1 The Annual License Fee

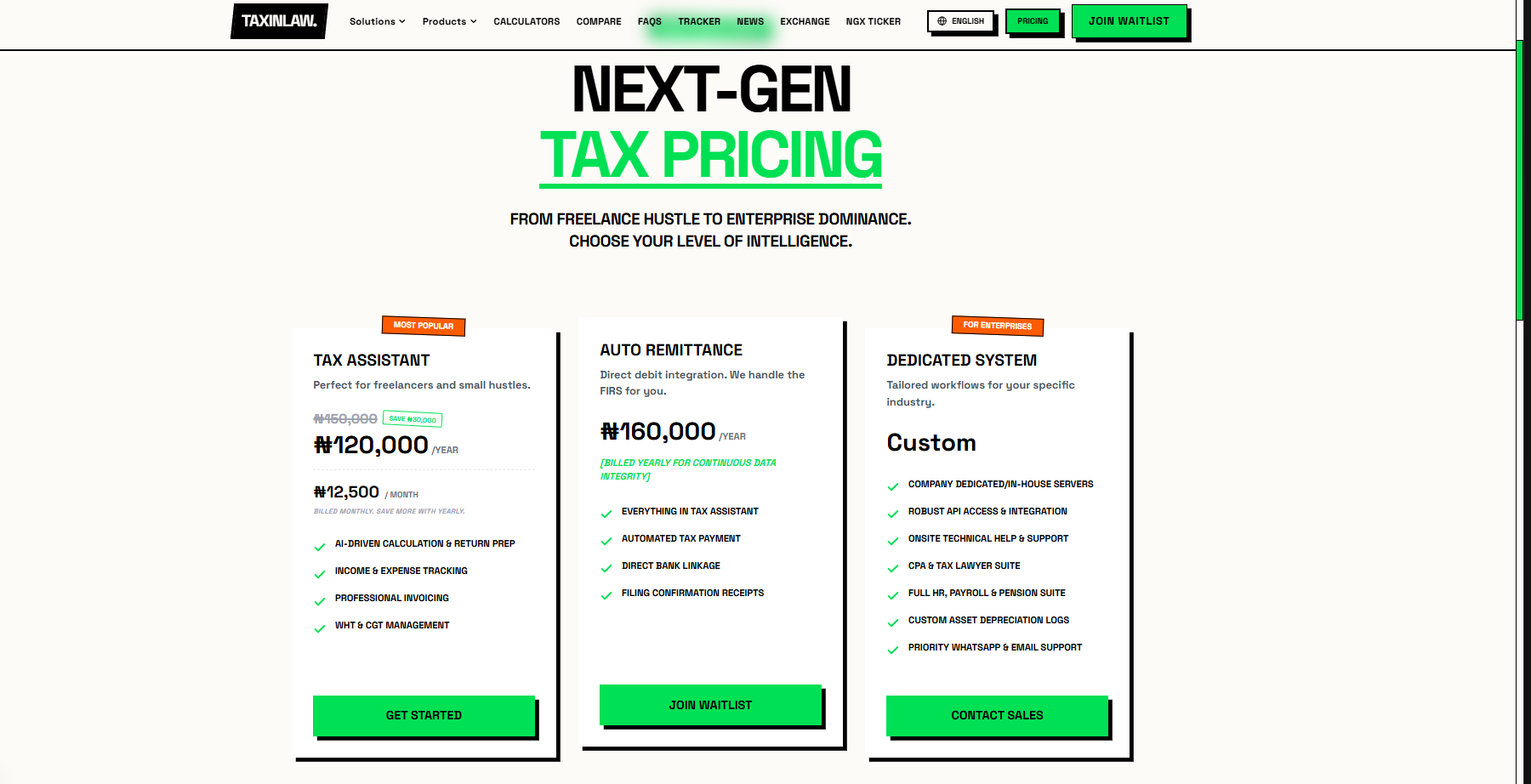

The TaxInLaw Business platform is offered to end-user Clients at an Annual License Fee of ₦120,000 (One Hundred and Twenty Thousand Naira) per entity per annum. Current pricing information is publicly available at taxinlaw.com/pricing.

TaxInLaw reserves the right to adjust its publicly listed pricing. Commission calculations for Partners shall always be based on the actual verified received amount for any given Client at the time of activation, not on any projected or estimated figure.

3.2 Commission Structure — Foundational Principles

We want to be upfront about something: TaxInLaw is a technology company with real infrastructure costs — cloud servers, security architecture, regulatory compliance engineering, ongoing product development, customer success operations, and legal overhead. We are committed to paying our Partners fairly and competitively. We are equally committed to not pricing ourselves into an unsustainable operating position. The commission structure below reflects that balance honestly.

TaxInLaw shall retain a minimum of seventy percent (70%) of every Annual License Fee received, at all times, under all circumstances, regardless of tier, renewal status, or any other factor. The Partner's maximum entitlement, inclusive of all commissions of any type, shall never exceed thirty percent (30%) of the Annual License Fee.

This is not a negotiating position. It is a structural requirement for TaxInLaw's continued ability to deliver and improve the platform your Clients are relying on.

3.3 Tiered Commission Schedule — New Client Onboarding

Tier Progression: Tier upgrades are applied prospectively upon each verified successful Client onboarding that crosses a tier threshold. Upgrades are not retroactive to prior activations. A Partner at Silver tier who activates their 16th Client is elevated to Gold from that activation onward — the prior 15 activations are not recalculated.

Tier Retention: Tiers shall not be downgraded within the first twelve (12) months of active Partner status. Annual reassessment may occur thereafter based on continued Program engagement.

Absolute Cap — Reiterated for Clarity: No commission of any type — new client, renewal, bonus, or otherwise — shall exceed thirty percent (30%) of the Annual License Fee, under any interpretation of this Proposal or any subsequent Agreement.

3.4 Renewal Commission

TaxInLaw recognizes that retaining a Client is commercially valuable and that the Partner who built that Client relationship often plays a meaningful role in ensuring renewal. Accordingly, Authorized Partners are entitled to a commission on Client license renewals under the following terms:

- ›• The renewal commission rate shall be the Partner's standard tier rate at the time of renewal, capped absolutely at thirty percent (30%) — consistent with the Program's universal commission ceiling.

- ›• Renewal commissions are payable only where:

- ›• (i) TaxInLaw receives the Client's renewal payment in full and confirmed;

- ›• (ii) The renewal occurs within sixty (60) days of license expiry;

- ›• (iii) The Partner remains in good standing under the Program;

- ›• (iv) The Partner has engaged meaningfully with the Client's account within the ninety (90) days preceding renewal (as evidenced by Portal activity, communication records, or documented renewal outreach).

- ›• No renewal commission shall be payable where the Client independently initiates and completes renewal directly with TaxInLaw, without any documented participation or outreach by the Partner in the preceding ninety (90) days.

- ›• TaxInLaw retains the right to engage directly with any Client to support, encourage, or facilitate renewal at any time, as platform continuity and Client success are primary operating priorities of TaxInLaw — not secondary responsibilities.

- ›• TaxInLaw retains a minimum of seventy percent (70%) of all renewal revenue. The Partner's renewal commission shall never cause TaxInLaw's retained share to fall below this threshold.

3.5 Commission Disbursement

All commission payments are subject to prior, verified receipt of the Client's Annual License Fee by TaxInLaw. Commissions shall be disbursed pursuant to the schedule and mechanics to be defined in the Channel Partner Agreement, which shall include provisions for a standard disbursement cycle, minimum thresholds, and required Partner documentation.

SECTION IV — THE TRANSACTION WORKFLOW

4.1 The Full Process — Step by Step

The following workflow governs every Partner-initiated Client sale under the Program. There are no shortcuts. Every step exists for a reason, and deviation from this process constitutes a procedural breach:

STEP 1 — SALE

Partner identifies a prospective Client and presents TaxInLaw's offering.

Partner confirms Client eligibility and intent to purchase.

STEP 2 — COLLECTION

Partner collects the full Annual License Fee (₦120,000) from the Client.

The Partner may collect the full amount and remit TaxInLaw's share,

or agree with TaxInLaw on a direct-to-TaxInLaw collection structure

(to be defined per arrangement in the Agreement).

STEP 3 — REMITTANCE

Partner transfers TaxInLaw's share (minimum 70% of ₦120,000 = ₦84,000)

to TaxInLaw's officially designated receiving account as published

exclusively on the TaxInLaw Partner Portal.

STEP 4 — CLIENT INFORMATION PACKAGE

Partner submits the Client Information Package to TaxInLaw simultaneously

with the transfer (details in Section 4.2 below).

STEP 5 — VERIFICATION

TaxInLaw cross-references the payment against its bank records and the

submitted Client information. Verification SLA: 48 business hours.

STEP 6 — ACCOUNT CREATION & ACTIVATION

TaxInLaw creates the Client's account and generates a secure license key.

STEP 7 — LICENSE KEY DELIVERY

TaxInLaw transmits the license key to the Partner via official channels.

STEP 8 — CLIENT HANDOVER

Partner delivers the license key to the Client and facilitates initial onboarding.

STEP 9 — RECORD LOGGING

Both TaxInLaw and the Partner record the completed transaction in the

TaxInLaw Partner Portal. The record is permanent and immutable.

4.2 Client Information Package

The following information must be included in the bank transfer description and submitted simultaneously through the TaxInLaw Partner Portal:

- ›• Full legal name of the Client entity (as registered with the CAC)

- ›• Client's Tax Identification Number (TIN) and/or CAC Registration Number

- ›• Client's primary contact name and email address

- ›• Client's active phone number

- ›• Partner's registered name and assigned Partner Reference Code

- ›• License term (Annual — 12 months)

Failure to include complete Client information in the transfer description or to submit it through the Partner Portal on the same business day as the transfer is a procedural breach that delays verification and activation. TaxInLaw assumes no liability for delays caused by incomplete or inaccurate Partner submissions.

4.3 Payment Verification Standards

TaxInLaw shall verify all remittances through a minimum of three (3) independent sources:

- ›TaxInLaw's own bank statement — confirming credit of the remitted amount;

- ›Third-party transaction records — where the transfer is processed through a recognized banking institution or licensed fintech platform (e.g., GTBank, Access Bank, Zenith, UBA, Flutterwave, Paystack, Interswitch), the transaction reference number shall be cross-checked where available;

- ›Transfer Description Matching — the Client's name and/or TIN as included in the transfer must correspond with the submitted Client Information Package.

Supporting documentation (debit alerts, digital receipts, fintech confirmation screenshots) is welcome and may expedite verification, but is not, of itself, conclusive proof of receipt. Receipt is confirmed solely by credit as reflected in TaxInLaw's verified bank statement. No other source of confirmation — including any verbal representation by a bank agent, a pending transaction notification, or a Partner's own remittance record — shall constitute confirmed receipt for the purposes of license activation.

As TaxInLaw scales its operations, the Company expects to implement progressively advanced verification infrastructure — including automated transaction reconciliation, third-party API integrations with banking providers, and, in future enterprise-grade deployments, barcode and QR-code enabled transaction matching systems — that will substantially reduce verification time and eliminate manual reconciliation steps.

4.4 48-Hour Verification SLA

TaxInLaw commits to completing payment verification and license key generation within forty-eight (48) business hours from the later of:

- ›• (i) Confirmed credit of funds in TaxInLaw's designated account, or

- ›• (ii) Receipt of a complete and valid Client Information Package.

This SLA applies during standard Nigerian business days (Monday through Friday, excluding public holidays). TaxInLaw will make reasonable commercial efforts to improve this SLA over time as verification infrastructure matures.

SECTION V — PAYMENT DISPUTES: WHAT HAPPENS WHEN MONEY DOESN'T ARRIVE

5.1 The Principle of Financial Responsibility

Let us be direct about something that is foundational to this entire Program: TaxInLaw Technology Limited is a software company. We are not a bank. We are not a payment processor. We are not an escrow agent. We do not handle, hold, intermediate, or insure the movement of money between the Partner and the Client.

The Partner assumes exclusive, full, and primary financial responsibility for all monetary transactions in the Partner-to-TaxInLaw and Client-to-Partner legs of every transaction. The moment a Partner agrees to collect payment from a Client on TaxInLaw's behalf, the Partner has taken on a financial obligation that TaxInLaw has not asked to share.

This is not a punitive stance. It is a structural reality. TaxInLaw's obligation is clear: when we receive confirmed funds and valid Client information, we create the account and issue the license key — within 48 business hours. Everything upstream of that is the Partner's domain.

5.2 Formal Dispute Process

In the event a Partner asserts that payment has been remitted but TaxInLaw's records do not reflect receipt, the following process governs:

Within twenty-four (24) hours of alleged remittance, the Partner must submit a formal Payment Dispute Notice to

taxinlaw@proton.me containing:

- ›• (a) A certified copy of the bank debit confirmation (not a screenshot alone — a document verifiable with the issuing institution);

- ›• (b) The full transaction reference number;

- ›• (c) The exact receiving account details to which the transfer was directed;

- ›• (d) The date, time, and amount of the transfer;

- ›• (e) The name of the financial institution used.

Within seventy-two (72) business hours of receiving a complete dispute notice, TaxInLaw shall conduct an internal reconciliation review.

5.3 Outcomes of Dispute Investigation

The following scenarios and their consequences are defined in advance to eliminate ambiguity:

Scenario A — Transfer to Wrong Account Number: Where investigation confirms that the Partner transmitted funds to an account number that is not TaxInLaw's officially designated receiving account (as published on the Partner Portal at the time of transfer), the loss rests entirely and exclusively with the Partner. TaxInLaw bears zero liability for funds transmitted to an incorrect, unauthorized, or fraudulent account, regardless of how the Partner came to possess that account number. It is the Partner's non-delegable obligation to verify TaxInLaw's receiving account directly through the Partner Portal before every transfer.

Scenario B — Confirmed Legitimate Bank Error: Where both parties can establish through official correspondence with the relevant banking institution that a bona fide technical bank error occurred, both parties shall cooperate in good faith to pursue resolution through that institution's dispute process. TaxInLaw's obligation to issue a license key remains suspended until funds are confirmed received.

Scenario C — Funds Received But Not Yet Credited: Where TaxInLaw's bank confirms a transaction is in processing, TaxInLaw shall extend reasonable cooperation and shall complete activation within 48 business hours of credit confirmation.

In all scenarios, TaxInLaw shall not issue a license key on the basis of an unconfirmed, disputed, or pending payment claim. Any Partner who makes representations to a Client about license access prior to confirmed activation shall do so at their own commercial risk.

SECTION VI — FRAUD PROTECTION & LIABILITY FRAMEWORK

6.1 Partner's Client Due Diligence Obligation

Every Authorized Partner assumes a professional duty of reasonable care in assessing the identity and legitimacy of each Client they introduce to the Program. At minimum, this means:

- ›• Confirming that the Client is a registered business entity with a verifiable CAC number or active TIN;

- ›• Not knowingly facilitating access to the TaxInLaw platform for entities engaged in financial fraud, tax evasion, money laundering, or any other activity prohibited under the laws of the Federal Republic of Nigeria;

- ›• Exercising the same standard of due diligence you would apply to any professional client engagement within your own practice.

We are not asking you to be a regulatory authority. We are asking you to be a responsible professional.

6.2 Safe Harbour — Good Faith Partner Protection

TaxInLaw genuinely recognizes that a Partner operating in good faith may, despite reasonable efforts, unknowingly onboard a Client who later proves to be engaged in fraudulent activity. In such circumstances, where it is established by documentary evidence, cooperation with law enforcement, and sworn affidavit that:

- ›(a) The Partner conducted reasonable, documented verification of the Client's identity using publicly available records (e.g., CAC database, FIRS TIN Verification Portal);

- ›(b) The Partner received no benefit from the fraudulent scheme beyond their standard Program commission;

- ›(c) The Partner, upon discovery or reasonable suspicion, promptly notified TaxInLaw and relevant authorities, including the EFCC where warranted;

...TaxInLaw shall, at its sole discretion, elect to abstain from pursuing civil claims against the Partner and shall cooperate with any regulatory or law enforcement process to confirm the Partner's documented good-faith conduct.

This Safe Harbour provision is a good-faith commercial commitment at the proposal stage and shall be formalized with precise legal definition in the Channel Partner Agreement. It does not, and cannot, shield the Partner from criminal liability under Nigerian statutory law, which is exclusively governed by the courts of the Federal Republic of Nigeria.

6.3 Partner Complicity in Fraud — Consequences

Where credible evidence establishes that an Authorized Partner knowingly participated in, facilitated, or willfully disregarded obvious indicators of a Client's fraudulent conduct, TaxInLaw shall, without limitation:

- ›Immediately and permanently terminate the Partner's Program status, without notice, compensation, or cure period;

- ›Withhold and permanently forfeit all accrued but unpaid commissions;

- ›Pursue full civil restitution for all losses, costs, legal fees, reputational harm, and regulatory penalties incurred by TaxInLaw as a direct or proximate result of the Partner's conduct;

- ›Report the Partner to the EFCC, FIRS, the Central Bank of Nigeria (CBN), and all other relevant regulatory authorities with jurisdiction;

- ›Provide unrestricted access to all Platform transaction records, Partner Portal activity logs, and communications to law enforcement upon lawful request.

Partners should be aware that knowing involvement in fraudulent schemes may expose them to criminal liability under, among others:

- ›• Section 419, Nigerian Criminal Code Act — Obtaining property by false pretences

- ›• Sections 14–17, Money Laundering (Prevention and Prohibition) Act 2022 — Concealment and conversion of proceeds of unlawful activity

- ›• Section 14(1), EFCC (Establishment) Act — Fraud-related offences

- ›• Sections 6 and 14, Cybercrimes (Prohibition, Prevention, Etc.) Act 2015 — Computer and identity fraud

- ›• Where applicable by jurisdictional reach: 18 U.S.C. § 1343 (Federal Wire Fraud Act) and 18 U.S.C. §§ 1961–1968 (RICO Act, USA) — particularly relevant where transactions involve internationally incorporated entities, foreign-domiciled parties, or cross-border financial flows

Independent legal advice is strongly encouraged for any Partner with any uncertainty about a prospective Client's legitimacy before proceeding with a sale.

SECTION VII — THE TAXINLAW PARTNER DASHBOARD

7.1 Your Window Into Everything

One of TaxInLaw's core commitments under this Program is radical operational transparency. We believe Partners perform better, stay more engaged, and build more valuable client relationships when they have real, unfiltered visibility into their own Program activity. The TaxInLaw Partner Dashboard is the mechanism that delivers on that commitment.

Upon formal onboarding, each Authorized Partner is issued individual, non-shareable login credentials to a secure, role-restricted module of the TaxInLaw platform — the Partner Dashboard. The Dashboard is currently in active engineering development, and its rollout is a near-term priority on TaxInLaw's product roadmap. The operational features it will deliver include:

Feature What It Does For You

Client Ledger See every Client you've onboarded: their legal name, plan type, activation

date, subscription expiry, and current renewal status — all in real time

License Code Inventory Monitor your full inventory of issued, unused, and redeemed license keys.

Know exactly what you have to work with before a Partner call

Commission Statements Itemized, timestamped records of every commission earned, pending, and

disbursed. Fully transparent, fully auditable

Renewal Alert Centre Automated notifications at 60, 30, and 7 days before each Client's license

expires — so you never miss a renewal conversation

Code Batch Request Submit formal requests for additional license key batches directly through the

Portal, subject to TaxInLaw approval

Document Hub Access TaxInLaw's official marketing materials, product documentation, and

Program updates — all current, all approved

7.2 Exclusive Client Registration — Resolving Conflicts Before They Start

In any active Partner network, the risk exists that two Partners may independently approach the same prospective Client. TaxInLaw addresses this proactively through the Client Priority Registration System:

- ›• The first Partner to formally register a named prospective Client through the Portal holds priority commission claim on that Client for ninety (90) days from registration date;

- ›• If no verified sale is completed within ninety (90) days, the registration lapses automatically, releasing the Client for registration by any other Partner;

- ›• Commission on any Client is payable to one Partner only — the Partner of record at the time of verified payment. No shared or split commissions shall be issued;

- ›• TaxInLaw's administrative determination of Partner of record is final and binding, subject to the formal dispute resolution mechanism defined in the Channel Partner Agreement.

7.3 License Key Security — Non-Negotiable Rules

TaxInLaw's license keys and platform passcodes are proprietary digital assets. Authorization to distribute them to a specific, verified Client does not convey any right to redistribute, reassign, resell, or share them further. Authorized Partners are expressly prohibited from:

- ›• Distributing license keys to any party other than the verified, named Client for whom the key was issued;

- ›• Sharing Partner Portal credentials with any individual within or outside the Partner firm who has not been expressly authorized by TaxInLaw;

- ›• Attempting to replicate, reverse-engineer, decompile, or reproduce any component of the TaxInLaw platform;

- ›• Selling, leasing, sublicensing, or otherwise commercializing license keys in any manner inconsistent with the Program terms.

Violation of any of the above constitutes immediate grounds for termination and may give rise to civil liability under the Copyright Act 2022 (Nigeria) and criminal liability under the Cybercrimes (Prohibition, Prevention, Etc.) Act 2015.

SECTION VIII — CLIENT SUPPORT & ONBOARDING

8.1 Who Does What

A critical question for every Partner entering this Program is: "Once a Client has their license key, what happens? Who helps them? What am I responsible for?" The table below answers that clearly:

8.2 TaxInLaw's Support Commitment to Your Clients

TaxInLaw is directly invested in every Client's success — because Client retention is TaxInLaw's revenue, not just yours. TaxInLaw shall provide Clients with access to:

- ›• Comprehensive in-platform documentation and feature guides

- ›• The TaxInLaw Tutorial module embedded within the platform

- ›• Direct technical support escalation via official support channels (

taxinlaw@proton.me)

- ›• Regular platform updates aligned with FIRS regulatory changes, Finance Act amendments, and tax law developments

8.3 Client Complaints — TaxInLaw's Commitment and Its Limits

What TaxInLaw stands behind:

- ›• The platform shall function materially in accordance with its published feature set;

- ›• Service interruptions attributable to TaxInLaw's own infrastructure shall be addressed with commercially reasonable urgency;

- ›• Tax computation outputs shall reflect the rules encoded in TaxInLaw's engine at the version active at the time of computation;

- ›• Client data shall be protected in accordance with the Nigeria Data Protection Act (NDPA) 2023 and TaxInLaw's Privacy Policy.

What is outside TaxInLaw's liability:

- ›• Service interruptions caused by Nigerian internet service providers, power infrastructure, or the Client's own device or network;

- ›• Tax outcomes resulting from incorrect data inputted by the Client;

- ›• Regulatory penalties arising from the Client's own prior non-compliance before platform adoption;

- ›• Decisions made by the Client or their advisors based on platform outputs that were applied without appropriate professional judgment.

Partners shall not: Make any warranty, guarantee, or legal representation to a Client about the outcome of any tax filing or regulatory audit based on platform use. The platform is a compliance management and intelligence tool — it is not a substitute for professional tax counsel where specific, complex, or contentious matters are involved.

SECTION IX — RENEWAL TRACKING

TaxInLaw acknowledges that manual renewal management is operationally unsustainable as the Partner network grows. The Renewal Alert Centre within the Partner Dashboard is specifically designed to solve this. Until the Dashboard is fully deployed, Partners should maintain direct awareness of their Clients' expiry dates as visible in the Client Ledger. TaxInLaw shall support renewal tracking through a shared operational process to be detailed in the Channel Partner Agreement.

SECTION X — PROGRAM CONDUCT, RISKS, AND MUTUAL PROTECTIONS

10.1 Brand and Representation Standards

The Authorized Partner shall, at all times:

- ›• Represent TaxInLaw's features, licensing terms, and pricing only as stated in TaxInLaw's official materials;

- ›• Submit all proposed marketing materials referencing TaxInLaw to

taxinlaw@proton.me for written approval before publication or distribution;

- ›• Clearly identify themselves in all sales communications as an "Authorized TaxInLaw Channel Partner" and not as an employee, officer, or legal representative of TaxInLaw;

- ›• Refrain from making comparisons with competitor products that are not factually supportable.

Any breach of the above that results in a Client complaint, regulatory inquiry, media attention, or measurable reputational harm to TaxInLaw shall render the Partner liable for all associated costs and damages.

10.2 Known Program Risks and How We Address Them

The following risks are real. We name them here not to be alarmist, but because identifying them clearly is the first step in managing them together:

Risk Mitigation Mechanism

Partner remits payment but TaxInLaw doesn't receive funds Triple verification process; license issuance strictly contingent on confirmed

bank credit. Partner bears full financial responsibility.

Partner misrepresents the platform to close a sale Brand representation standards in this Proposal and in the Agreement;

TaxInLaw's direct Client support channel provides an independent accuracy

check.

Two Partners claim commission on the same Client Client Priority Registration System; Partner of record at payment time is the

sole commission recipient; TaxInLaw's determination is final.

Partner loses motivation after early sales Tiered commission structure rewards volume growth; Renewal commissions

create passive long-term income incentive.

Client contacts TaxInLaw directly, bypassing Partner TaxInLaw's support relationship with Clients is direct and intentional

it improves retention. Partners are reminded that renewal outreach is

their primary commercial responsibility; TaxInLaw contacting a Client for

support does not diminish the Partner's commission rights.

License keys redistributed outside authorized Clients Single-use code architecture; Portal inventory tracking; IP and cybercrime

legal protections.

Operational breakdown at high Partner volume Partner Dashboard engineering, automated verification SLA improvements,

and structured escalation channels (documented in the Agreement) are all

designed as scale-ready infrastructure.

10.3 Non-Solicitation

For the duration of Program participation and twelve (12) months thereafter, the Partner shall not use information obtained through the Portal or Program to divert any TaxInLaw Client to a competing software platform or service.

10.4 Inactive Status

Partners with no verified Client activation in any rolling six-month period shall be placed on Inactive Status. This does not terminate the relationship but restricts new license key allocations until activity resumes.

SECTION XI — ACCEPTANCE AND NEXT STEPS

If this Proposal reflects a Program you want to be part of, we'd love to move forward. Here's how:

Step 1 — Indicate Acceptance Send a written confirmation of your intent to proceed to

taxinlaw@proton.me with the subject line: "Channel Partner Acceptance — [Your Firm Name]."

Step 2 — Submit Supporting Information Include in your acceptance email:

- ›• Your firm's full legal name and CAC registration number

- ›• Name and title of authorized signatory

- ›• Primary point of contact name, email, and phone number

- ›• A brief description of your client base and distribution focus

Step 3 — Await the Channel Partner Agreement TaxInLaw shall issue the formal Channel Partner Agreement within ten (10) business days of receiving your complete acceptance. The Agreement will incorporate all terms from this Proposal and address the additional items deferred to the contract stage.

Step 4 — Onboarding Upon Agreement execution, TaxInLaw will set up your Partner Portal credentials, assign your Partner Reference Code, and issue your initial license key inventory.

CLOSING STATEMENT

The Nigerian business community is underserved when it comes to accessible, high-quality, technology-driven tax compliance tools. TaxInLaw was built to change that — and the Channel Partner Program is how we reach every corner of the market that our direct team cannot. We believe the Partners who join this Program in its early stages are making a strategic bet that will compound favorably as the platform and the Partner network grow together.

We've been transparent with you throughout this document — about what we pay, what we require, what we'll protect you from, and what you'll be responsible for. That transparency is not a legal strategy. It is the only way we know how to build partnerships that last.

We look forward to working with you.

TAXINLAW TECHNOLOGY LIMITED Authorized Signatory: ___________________________ Name: ___________________________ Title: ___________________________ Date: ___________________________

PROSPECTIVE PARTNER (Acknowledgment of Receipt and Review) Authorized Signatory: ___________________________

Name: ___________________________ Title: ___________________________ Date: ___________________________ Firm Name: ___________________________ CAC Registration No.: ___________________________ Email: ___________________________

This document is private and confidential. It is intended solely for the named Prospective Partner and their authorized legal counsel. Unauthorized disclosure, reproduction, or distribution is strictly prohibited. Contact:

taxinlaw@proton.me | © TaxInLaw Technology Limited. All rights reserved.

Ready to Apply?

Subject line: “Channel Partner Acceptance — [Your Firm Name]”

taxinlaw@proton.me© TaxInLaw Technology Limited. Private & Confidential.